| Empfehlungen |  |

Corporate Governance

|

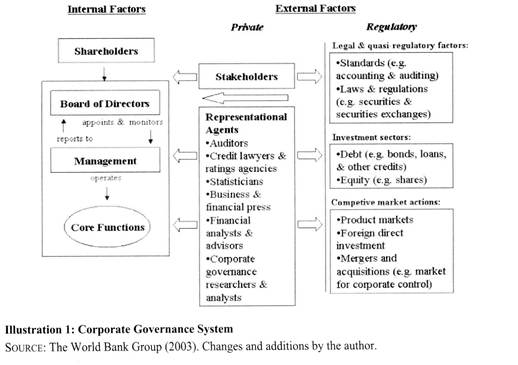

1. Characterization Corporate Governance is the system for directing and controlling corporations, especially those firms whose shares are publicly traded, through the reviewing, monitoring, disciplining, and rewarding of executive managers. The main objective of Corporate Governance is the protection of the valid interests of all stakeholders, who are the internal and external societal actors directly involved with or indirectly affected by the firm. The Board ofDirectors stands as the central actor in the system between the executive managers and the shareholding owners. See Illustration 1. 2. The Development of Principles of Corporate Governance Following the great crash of the USA securities markets in 1929, researchers A.A. Berle and G.C. Means observed the problem of the separation of ownership from control in modern corporations, a concept that is commonly labelled agency theory. Further to this theory, M.C. Jensen und W.H. Meckling classified three forms of agency costs: monitoring, bonding, and residual losses. Corporation must reckon with agency costs in order to attempt to minimize the expected conflicts of interest which exist between shareholders and management. Corporate leaders from the board of directors and from the executive managers are required to support monitoring through the deliberate installation and Operation of an appropriate intemal system of controls, reviews, and audits. Bonding is furthered through the linkage of shared decisions regarding strategy and resource allocation of the firm. Corporate leaders must strive to achieve the optimal weighting of investments between these two classes of agency costs, or they must accept a higher risk-level for the firm, which can lead to residual losses. Conflicts of interests are also reduced through achieving a higher level of information transparency. The quantity of information disclosures must meet minimum standards imposed by law or statute. For example, the European Union (EU) requires large publicly-traded corporations to disclose their financial results quarterly and all corporations to submit complete, detailed financial statements annually to their respective regulators. The quality of information disclosures is determined by their usefulness and timeliness. Financial statements of EU publicly-traded corporations, therefore, must comply with the true and fair view principle of the International Financial Reporting System (IFRS), the generally accepted accounting standards endorsed by EU regulators. At the turn of the 21s1 century, interested international organizations, e.g. the Organisation for Economic Co-operation and Development (OECD), sponsored and published recommended principles of corporate govemance. Many national legislators and securities exchanges followed with their own set of legally-binding rules. 3. Important Participants of the International Corporate Governance System (1) Board ofDirectors The board of directors is the legally-required supervisory organ in each corporation responsible for directing and controlling the firm. Appointing, advising, and leading the executive managers are important activities included among the board\'s responsibilities. In addition, the directors possess mature experiences, relationships, ideas, and other personal and professional abilities, so-called board capital, which they can bring to the benefit of the corporation. The leader of the board of directors is the chairman or chairperson, who directs the planning, administration, and calendar of the board and presides over official board meetings. (2) Executive Managers The executive managers are the group of officers who are at the pinnacle of the management hierarchy of the organization. This group is led by the chief executive officer (president or managing director) and by the chief financial officer (vice president of finance or finance director). Further members of executive management can include the heads of core functions of the business: operations, sales, marketing, human resources, etc. and the managing directors of subsidiary companies. The board of directors approves the appointment of all officers. (3) Committees of the Board of irectors The detailed responsibilities of the board of directors are often divided among and delegated to various committees, which are smaller workgroups normally made up exclusively of members of the board of directors. In most situations, the fall board of directors itself maintains final decision authority over the committees. The audit committee monitors the internal controls, contracts with or installs the external auditors, and approves the financial statements. A risk management committee is established in banks and financial services providers (as well as in some other corporations at their own discretion). This committee reviews whether the risks of investments and of operations are identified and weighted and that sufficient measures of risk avoidance and coverage (e.g. cash reserves; credit, transportation, property, and liability insurance; hedging contracts; balanced portfolios; liens on buildings, inventory, investments, and other assets; etc.) are implemented and functioning properly. The nominations committee recruits the chief executive officer (CEO) and new members to the board of directors and reviews the appointments of all executive managers, and the compensation committee develops and recommends all of the various elements which make-up their remuneration. (4) Shareholders In most public corporations there are numerous unrelated owners, generally called shareholders (or stockholders). This heightens the requirement for information transparency in disclosures made to them. The board of directors is legally required to invite all shareholders to an annual general meeting. In some situations, the shareholders must also be called to additional special meetings. The concept of one share — one vote for all shareholders is generally preferred for its transparent and fair division of rights based solely on firm ownership percentage. A majority of shareholders\' votes is normally required to approve the most critical strategic decisions affecting the firm, e.g. transacting new emissions of shares, establishing new ciasses of shares, electing new directors as well as the chairperson of the board, approving mergers and acquisitions, changing the corporation\'s Charter or the bylaws goveming the board of directors, approving significant new investments, etc. It is well accepted that shareholders do not have to be present in-person at a meeting for their votes to be counted. They can submit their votes via the postal service as well as by electronic (i.e. internet) voting methods. (5) Stakeholders Internat stakeholders include shareholders, managers, and employees. They are not the only actors who hold interests in the activities and results of the corporation. Stakeholders can also be private and public external parties who directly interact with or are indirectly affected by the firm. These extemal actors include customers, consumers, suppliers, subcontractors, creditors, debtors, unions, govemment officials such as securities exchange regulators, citizens in neighboring communities, etc. (6) Representational Agents Many third-party service providers act as representational agents who fulfill critical watchdog rolls through their analysis of and reporting on the corporation\'s actions. These primarily independent agents include extemal auditors, debt rating agencies, the business and financial press, investment researchers and consultants (financial analysts), various private, public, and quasi-public statisticiaris, etc. Their authority can be derived from direct legal provisions or from professional standards. (7) Regulatory Authorities Corporate leaders are required under regulatory authorities - by law, regulation, or accepted business practices - to perform their duties responsibiy and completely. Competitive product markets and financial markets, including investors and 1enders, exert additional pressures to control and influence the behavior and perfonnance of corporate leaders. This market for corporate control acts through the change of ownership interest, which can result in the takeover, merger, or insolvency of the firm. For the members of the board of directors and executive managers, this can lead to a dramatic reduction in their compensation, reassignment of their responsibilities, or reconsideration of the status of their appointments. 4. Important Provision for Germany, Austria, and Switzerland German, Austrian, and Swiss legislators have instituted a unique dual board system through the balanced legal positioning of the executive managers and the board of directors. Together, the internal management board (Vorstand in Germany and Austria, Geschäftsleitung in Switzerland) and the external supervisory board (Aufsichtsrat in Germany and Austria, Verwaltungsrat in Switzerland) lead the corporation. In all firms registered in Germany and Austria, and in all banks registered in Switzerland, the dual board system is mandatory. In the dual board system, members of the supervisory board must all be independent from the firm, e.g. managers and other employees of the firm cannot be members of the supervisory board. All members of the management board are actively employed officers of the corporation. Through the principle of co-determination (Mitbestimmungsprinzip), employees hold direct influence over the critical decisions of the firm, because they are given the right to elect members to the supervisory board. In most cases, employees have the right to elect a minimum of one-third of the members. In larger firms in Germany, e.g. those publicly-traded corporations with over 2000 employees, employees have the right to elect up to half of the members of the supervisory board. In these larger German firms, the chairperson of the board (Aufsichtsratvorsitzender) is elected only by the shareholders and holds two votes for board decisions, compared to one vote for all other board members. All non-bank Swiss corporations can choose to implement either a dual board or a unitary board of directors. In the unitary board system, which is the practice employed exclusively in most other countries, directors are elected only by the shareholders and can be either independent persons or executive managers. The chairperson (Präsident des Verwaltungsrates) holds one vote, the same as the other directors. The chairperson can also be the current CEO of the firm. Accepted Swiss standards of corporate governance, however, especially recommend CEO non-duality, where these two roles are separated and held by two individuals. Because it is not only possible but often the case that the board of directors holds some managers as members, the audit committee, by law, must include only independent members not employed by the firm. In addition, when the chairperson is also the CEO, boards often hold special meetings without the chairperson being present. The independent character of the directors in these special meetings should enable them as a group to measure and evaluate the performance and to set the compensation of the executive managers, without obvious conflicts of interest influencing these critical decisions.  Hinweis For related topics see Aktiengesellschaft, deutsche, Aktiengesellschaft, österreichische, Arbeitsrecht, Corporate Citizenship, Due Diligence, Gesellschaftsformen, österreichische, Gesellschaftsrecht, Europäisches, Hedgefonds, Interkulturelles Management, Lohn- und Gehaltsmodelle, Mergers & Acquisitions, Mittelstandsökonomie, Personalmanagement, Grundlagen, Personalmanagement, Internationales, Private Equity, Umweltmanagement, Unternehmensethik, Unternehmensführung. Hinweis For related topics see Aktiengesellschaft, deutsche, Aktiengesellschaft, österreichische, Arbeitsrecht, Corporate Citizenship, Due Diligence, Gesellschaftsformen, österreichische, Gesellschaftsrecht, Europäisches, Hedgefonds, Interkulturelles Management, Lohn- und Gehaltsmodelle, Mergers & Acquisitions, Mittelstandsökonomie, Personalmanagement, Grundlagen, Personalmanagement, Internationales, Private Equity, Umweltmanagement, Unternehmensethik, Unternehmensführung. Literatur: Colley, Jr., John L., Doyle, Jacqueline L., Logan, George W., Stettinius, Wallace (2003): Corporate Governance, McGraw-Hill, New York, USA; European Corporate Governance Institute (2006): Corporate Governance Codes, Principles and Recommendations, http://www.ecgi. org/codes/index.php January 8, 2006; Hilb, Martin (2006): Integrierte Corporate Governance. Ein neues Konzept der Unternehmensführung und Erfolgskontrolle, Springer, Berlin; Hoffmann, Dietrich und Preu, Peter (1999): Der Aufsichtsrat, 4. Auflage, C.H. Beck\'sche Verlagsbuchhandlung, München; Jensen, Michael C. und Meckling, William H. (1976): Theory of the Firm: Managertal Behavior, Agency Costs and Ownership Structure, Journal of Financial Economics, October, Vol. 3 No. 4, 305-360; Organisation für Wirtschafliche Zusammenarbeit und Entwicklung (2004): OECD-Grundsätze der Corporate Governance, Neufassung 2004, OECD, Paris, www.oecd.org/dataoecd/57/19/32159487.pdf January 8, 2006; Österreichischer Arbeitskreis für Corporate Governance (2006): Österreichischer Corporate Governance Kodex, Jänner, http://www.ecgi.org/codes/documents/accd_january2006_de.pdf October 7, 2006; Regierungskommission (2005): Deutscher Corporate Governance Kodex in der Fassung vom 2. Juni 2005, http://www.corporate-governance-code.de/ger/kodexiindex.htrn1 January 8, 2006; Solomon, Jill und Solomon, Ans (2004): Corporate Governance and Accountability, John Wiley & Sons, Chichester, West Sussex, England; The World Bank Group (2003) Corporate Governance: An Issue of Global Concern, http://www.worldbank.org,/html/fpd/privatesector/cg/aboutus.htm, March Internetadressen: http://www.oecd.org/topic/0,2686,en_2649_37439 1 1 1 1 37439,00.html; http:// www.ifc.org/ifcext/economics.nsf/Content/CG-Corporate_Governance_Department; http://www.ecgi.org/; http//vvww.ccg.ifpm.unisg.ch. Vorhergehender Fachbegriff: Corporate Finance | Nächster Fachbegriff: Corporate Governance Information and Forecasting Systems (CGIFOS) Diesen Artikel der Redaktion als fehlerhaft melden & zur Bearbeitung vormerken |

|

Schreiben Sie sich in unseren kostenlosen Newsletter ein

Bleiben Sie auf dem Laufenden über Neuigkeiten und Aktualisierungen bei unserem Wirtschaftslexikon, indem Sie unseren monatlichen Newsletter empfangen. Garantiert keine Werbung. Jederzeit mit einem Klick abbestellbar.

Weitere Begriffe : Solvabilitätsrichtlinie | automatische Datenverarbeitung | Streuplanung

|

Praxisnahe Definitionen Nutzen Sie die jeweilige Begriffserklärung bei Ihrer täglichen Arbeit. Jede Definition ist wesentlich umfangreicher angelegt als in einem gewöhnlichen Glossar. |

Fachbegriffe der Volkswirtschaft Die Volkswirtschaftslehre stellt einen Grossteil der Fachtermini vor, die Sie in diesem Lexikon finden werden. Viele Begriffe aus der Finanzwelt stehen im Schnittbereich von Betriebswirtschafts- und Volkswirtschaftslehre. |

Beliebte Artikel Bestimmte Erklärungen und Begriffsdefinitionen erfreuen sich bei unseren Lesern ganz besonderer Beliebtheit. Diese werden mehrmals pro Jahr aktualisiert. |